Apple's Service Business Could Be the Key to Its Future

Apple (NASDAQ: AAPL) has a new hit product -- and it's not the iPhone X

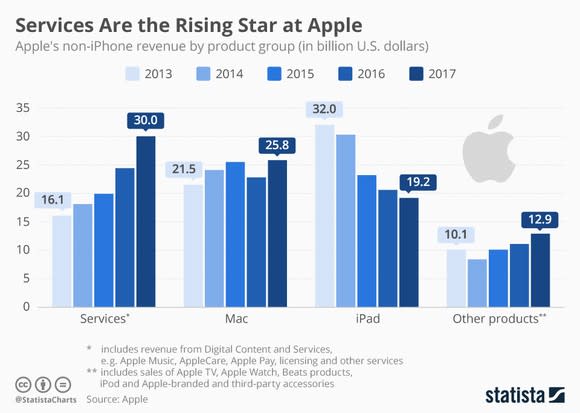

Apple Music, Apple Pay, iTunes, the App Store, iCloud, and Apple Care are all a part of Apple's services segment -- and services is now Apple's second-biggest "product." Revenue for the segment has more than doubled in the past four years, to over $30 billion.

When people think of Apple, they think of its hardware products -- the iPhone, iPad, and Mac. Sales of hardware, however, have stagnated, a victim of their own success and slowing upgrade cycles. Apple needs a new way to drive profit, and services might just be the ticket to future growth.

Image source: Statista

Apple's stock is cheap by any traditional valuation metric. Its forward price-to-earnings ratio is just 14, and it sports a dividend yield of 1.48%. And that's to say nothing of its cash and cash equivalents balance of $258.9 billion -- a huge sum that brings the company's valuation even lower. Bulls believe that the company's brand name is too strong, and its share price too cheap, to ignore. Its ecosystem is robust, and consumers view the company as a quality brand. Services provides Apple a way to both further monetize its ecosystem and make it stronger.Â

Image source: Getty Images.

Bears would argue that Apple needs the diversification. In its latest quarter, 54.86% of Apple's revenue came from iPhone sales, and that ratio has been as high as 70% in the past. Not only is Apple incredibly reliant on the iPhone for its profit, but the phone's enormous success also holds the keys to its potential doom: It's just too big. Any new products would have to be smashing successes, and that's no easy feat in the tech world. Moreover, the bears argue that if services continues to grow but hardware doesn't, Apple would be merely replacing hardware losses and essentially running in place.

For now, the weight of the evidence lends itself to the bull case, in that services growth is a leading indicator of future hardware sales. After all, if one owns an Apple TV, does personal computing on a Mac, and has a music library through Apple Music, that person is less likely to buy an Android or Windows product. The value of the ecosystem is simply too strong and the hassles of switching over just aren't worth it.

And for as big as the iPhone is, it still continues to be an innovative product. The latest versions, iPhone X and iPhone 8, have, among other attractive features, increased virtual-reality capabilities. It's not hard to imagine that the sale of virtual-reality games and applications through the App Store will generate a brisk business for Apple.

The Apple doesn't fall far from the (services) tree

Fears that Apple is just too big to move the profit-growth needle -- or, worse, that sales of hardware products could slide -- are warranted. Investors losing sleep over this point, however, should rest easier thanks to the services segment. Its gross margin is enormous, and the business continues to grow by leaps and bounds. As icing on the cake, its success only adds to the value of Apple's hardware business, in a hugely profitable positive feedback loop.

More From The Motley Fool

6 Years Later, 6 Charts That Show How Far Apple, Inc. Has Come Since Steve Jobs' Passing

Why You're Smart to Buy Shopify Inc. (US) -- Despite Citron's Report

Sean O'Reilly has no position in any of the stocks mentioned. The Motley Fool owns shares of and recommends Apple. The Motley Fool has the following options: long January 2020 $150 calls on Apple and short January 2020 $155 calls on Apple. The Motley Fool has a disclosure policy.